By Baptiste Albertone

The weight of the past has sometimes been more present than the present itself. And a repetition of the past has sometimes seemed to be the only foreseeable future.

Enrique Krauze

The history of independence in Latin America is a history of reproduction of the same, but different. The Napoleonic wars that weakened the Crown provided the opportunity for Latin American landlords to finally claim the full possession and administration of the fertile soil and abundant cheap labour at their disposal. As the first nations proclaimed their right to self-determination, the new states engaged in the consolidation of a new institutional framework, independent of the Crown, but reconfigured to fit the taste and interests of landed-elites and the colonial bourgeoisie. As it is common in the revolutionary processes of nations under colonial rule, despite the adhesion and (indispensable) active participation of the popular sectors, only a segment of the elite benefited from the structural reconfiguration of what the Marxist literature calls: a Bourgeois revolution.

The political rupture translated into economic continuity: The regime of accumulation inherited from the colonial period remained unaltered to reproduce a rentier-style capitalism. Indeed, the material reason for independence was not the transformation of the economic structure but the conquest of a larger share of its benefits by one class. In addition to internal interests, a parallel international driving force supported the maintenance of this rentier regime: the centro-peripheral dynamics of the world economy, which placed Latin American nations in a subordinate and “dependent” condition of natural resource providers for “core” economies.

The role of economic ideas has certainly been decisive in the ability of the rentier regime to reproduce itself despite its deleterious effects. First, in the post-independence period, the neoclassical theory of comparative advantage offered a strong argument against developing a manufacturing sector through industrial policy. Later, in the early post-war years, the US administration-backed modernization theoryacted as a strong counter-discourse to classical development theorists’ arguments in favour of a structural transformation. Finally, from the late 1970’s onward, the infamous Washington Consensus came to provide an intellectual rationale to the political and historical project of capital and power concentration with de-industrialisation in the Latin American continent.

The socio-economic consequences of the rentier developmental mode are profound. As the Latin American structuralist school has vastly discussed, the rent-seeking style of development has favoured the persistence of 1) a large pre-capitalist sector, and 2) a highly heterogeneous intersectoral productivity. These structural determinants have major consequences on both pre-tax and post-tax income inequality dynamics. First, the economic dualism of the productive structure, a feature of rentier capitalism, implies that the share of labour in national income is very low In fact, land concentration and the scarcity of productive employment produce structurally unequal labour markets, with a very high number of informal workers acting as a reserve army. Second, the absence of a meaningful social contract between the governing elites and the popular sector gives rise to a regressive and fragile fiscal state, reluctant to influence the structural level of inequalities and to finance public goods.

Therefore, the Latin American state was designed in such a way to guarantee the reproduction and the capture of the benefits of economic development by a wealthy minority, echoing Smith’s view that “[c]ivil government (…) is in reality instituted for the defence of the rich against the poor, or of those who have some property against those who have none at all”.

The so-called era of democratisation in Latin America did not alter these power asymmetries. The structural configuration of extreme wealth and income inequalities as well as an almost unlimited ability to match economic power with political power gave rise to a form of quintessential Neoliberal state where, in José Gabriel Palma’s words the “new ‘democratic’ agenda of capital ensures that the state will fulfill its sole function of reproducing the new capitalist system”. The consequence is a unique level of inequality characterised by an unrestricted capacity of the elites to perpetuate themselves despite political changes.

But if the recipe for Latin American success once appeared to be a well-kept secret – only shared with some South African nations – it may no longer be the case. The neoliberal revolution that successfully altered labour markets and fiscal structures of most OECD countries is producing what Palma describes as a form of “reverse catching up”, with some advanced economies moving towards a Latin American style of accumulation.

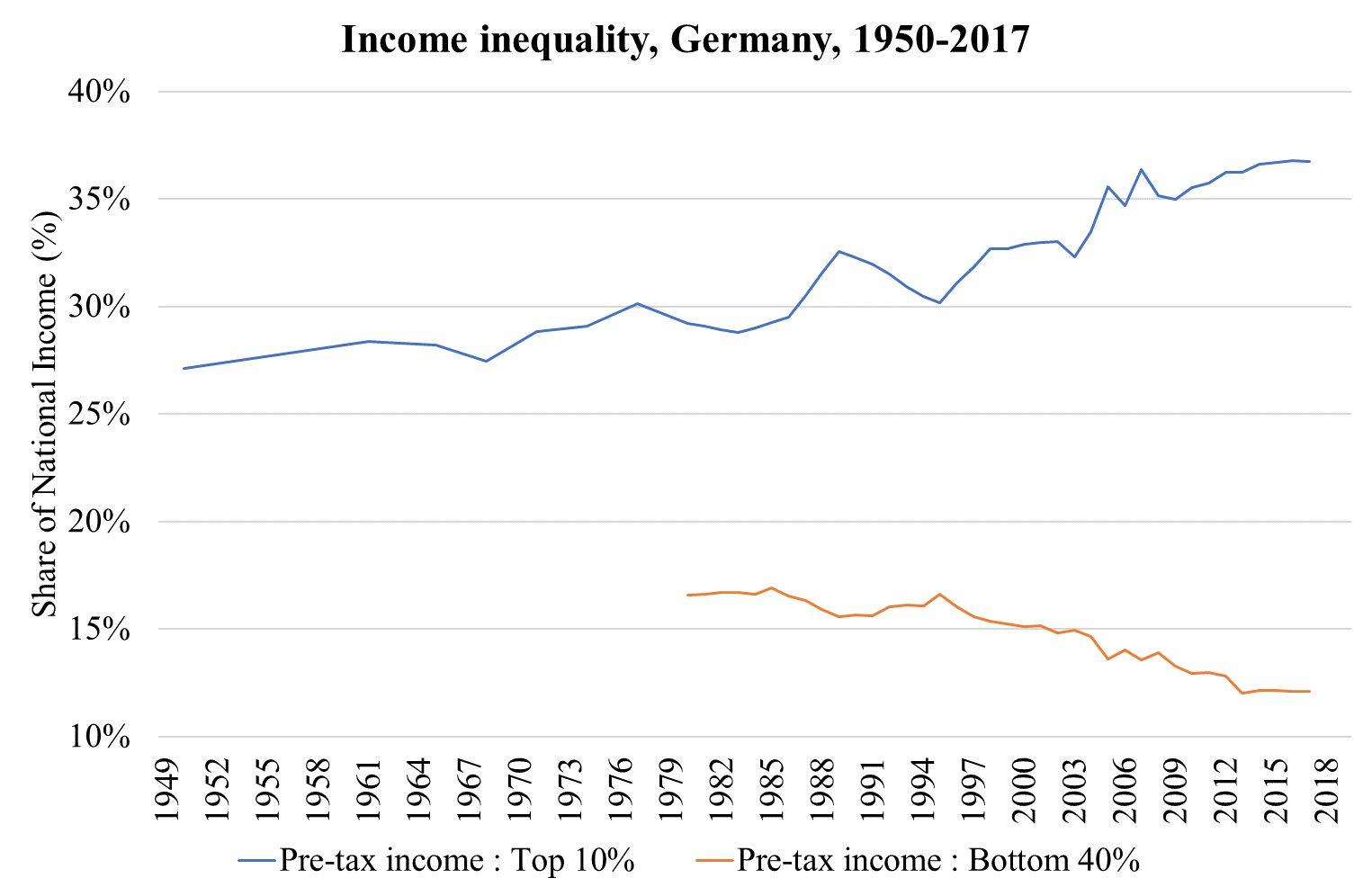

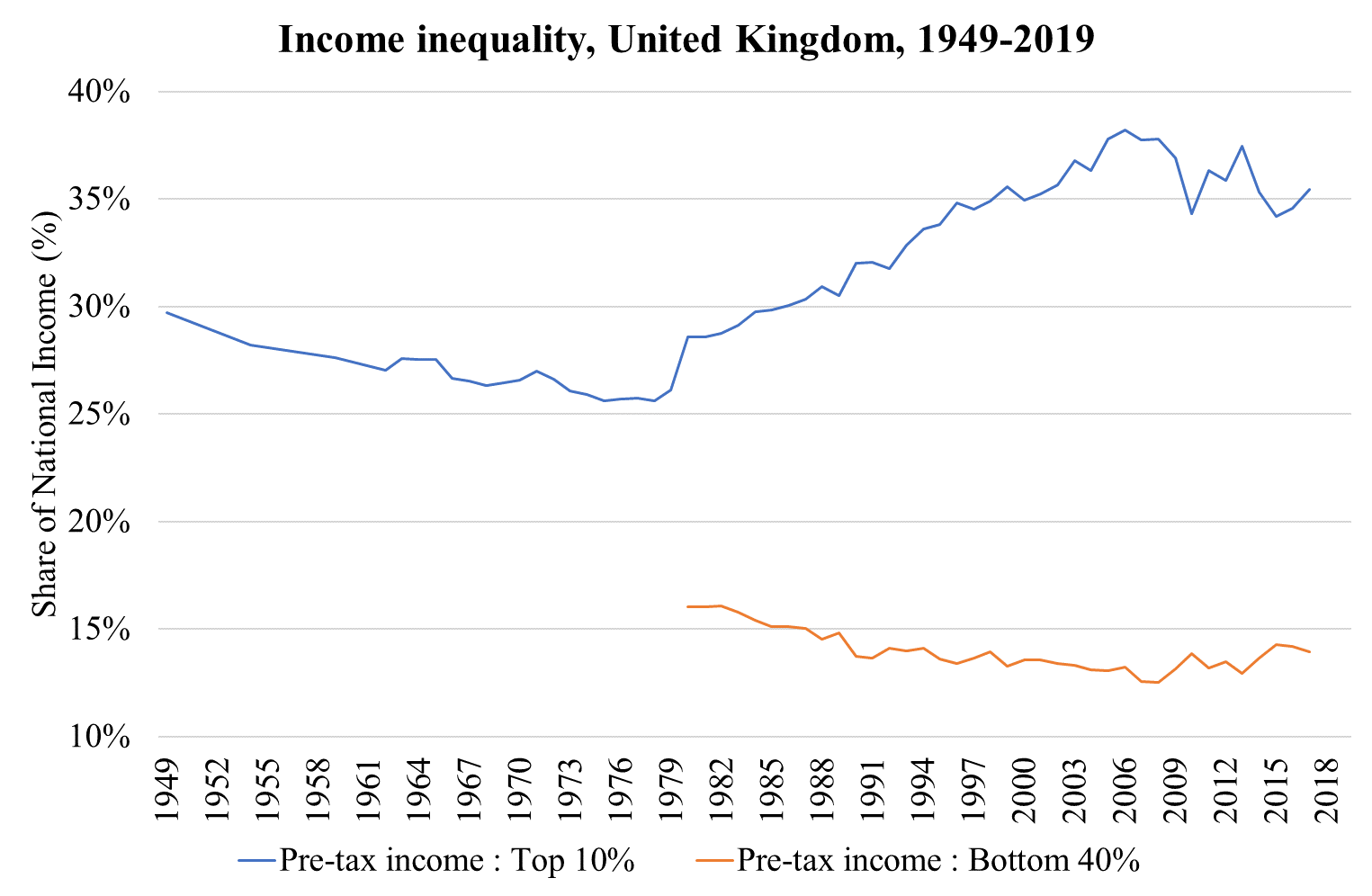

The graphs below illustrate the evolution of pre-tax inequalities in Germany, the United States, and the United Kingdom, three of the countries most affected by Neoliberal — or Ordoliberal in the German case — reforms.

Since the 1980s, these countries have experienced a dramatic rise in the share of the national income going to the individuals in the top 10% of the income distribution, mirrored by an almost identical, but opposite, trend affecting the share held by the bottom 40%. These tendencies are certainly not independent of the political and economic context that characterised the period.

From the mainstream viewpoint, the justification given for the tragic evolution of inequality is that of an growing capital-output ratio driven by entrepreneurial investment leading to an elevation in the share of profits in national income.

Nonetheless, when looking at real investments’ figures, the picture turns out to be dramatically different from the expected dynamic. In the US, the gross private investment share of GDP has fallen by 3 percentage points since the late 1970s. On the contrary, what we see is a growing capacity from corporate elites to capture the benefits of economic growth with the help of both globalisation and financialization dynamics. Consequently, between the mid-1970’s and 2017, while real US GDP did more than triple, the real hourly wage of most Americans stagnated.

What is at stake is a reconfiguration of the political space in the image of the Latin American oligarchical institutional style, where hierarchical economic principles subordinate the democratic and representative principles of politics embodied in the figure of the State. According to Branko Milanovic, the neoliberal restructuring while “it maintained the pretence of equality (one-person one-vote), (…) eroded it through the ability of the rich to select, fund, and make elect the politicians friendly to their interests”. In other words, neoliberalism should be understood as an active project that, as Quinn Slobodian notes it, “rather than ‘freeing’ or ‘disembodying’ ‘the’ market, [attempt] an ‘encasement’ of economic structures, isolating them from popular democratic demands”.

By weakening the power of labour with more flexible workers’ protection, unravelling the Welfare State where it existed, engaging in a privatisation of public goods — the capital of those who don’t have any —, by adopting tax reforms that enhance regressive taxation and tax evasion, and by globally consolidating what Slobodian calls “the human right of capital flight”, neoliberalism demonstrated its striking effectiveness as a “technology of power” to rewrite the rules of the game in favour of capital accumulation. In the same way as Latin-American elites structured the newly born nation for the benefits of their interests, the recent success of Northern capitalist elites to create an environment suitable for the flourishing of their rent-extraction ambitions.

The structural reconfiguration that has been taking place since the mid-1970s is simultaneously endangering social and ecological balances, as well as putting societies at risk of implosion under authoritarian governments eager to establish Neoliberalism in a single country. We might be heading towards a dark horizon sketched by Slobodian as one of “brute competition in a zero-sum world where all that matters is the enrichment of an ethnically defined, territorially bounded national population”, where the protection of the environment – a common good by definition – is relegated to the tenebrous depths of national political agenda.

From this frightening observation arises an unsurpassable necessity to engage in a struggle for the transformation of economics — which today serves under its technocratic authority as the core instrument of the corporate elites’ political project — so that it becomes a democratic instrument for a fair and ecological economic transformation.

About the author: Baptiste Albertone is an MPhil candidate in Development Studies at the University of Cambridge and holds an MA and BA from the Institut d’Etudes Politiques de Paris. His research focuses on industrial policy and sustainable development in the Latin American context. Twitter: @BaptAlbertone

This article is a runner up in an essay competition held by the UNCTAD YSI Summer School on Globalization and Development Strategies. Participants of the school worked with senior scholars to fine-tune their drafts, and the top-5 articles were published here. For other articles in the series, please click here.

About UNCTAD UNCTAD is a permanent intergovernmental body established by the United Nations General Assembly in 1964. Its headquarters are located in Geneva, Switzerland, with offices in New York and Addis Ababa. UNCTAD is part of the UN Secretariat, reports to the UN General Assembly and the Economic and Social Council, and are also part of the United Nations Development Group.